B2B Late Payment Crisis 2025

The B2B Late Payment Crisis No One Can Afford to Ignore

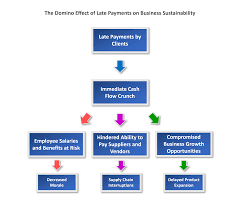

Late customer payments have quietly become one of the most expensive problems facing U.S. businesses. What used to be the exception is now the rule, and the ripple effects reach far beyond unpaid invoices.

In 2025, 55% of all B2B invoiced sales in the U.S. are past their due date, and the average business waits 43 days to receive payment. This isn’t just a minor accounts receivable hiccup—it’s a structural issue that impacts hiring, investment, daily operations, and long-term growth, with small business taking the biggest hit.

The Cost of Today’s Late Payment Practices

Behind the unpaid invoices on your accounts receivable aging is time, energy, and money tied up in follow-ups, recordkeeping, and uncertainty.

Here are some sobering statistics:

- The average small business is owed more than $17,000 in late payments

- 65% of businesses spend roughly 14 hours per week chasing overdue invoices.

- 79% of organizations experienced payment fraud attempts in 2024

Note: I found that last statistic so hard to believe I checked it with more than one AI – and here is what I got back:

Short answer: that figure is plausible and supported by a major industry survey. The 79% figure (organizations reporting attempted or actual payments-fraud activity in 2024) matches the Association for Financial Professionals’ 2025 Payments Fraud and Control Survey (which reports 79% for 2024). [1][2] (afponline.org)

The same AFP report also says checks were the payment type most often subjected to fraud (about 63% reporting check-related attempts), and industry commentary notes virtual/virtual-card solutions have stronger built-in controls and are generally considered safer than paper checks.

For 50 more statistics on delayed payments in 2025 (yes you read that right, in fact I think it’s 51 more you can read Dean Kaplan of The Kaplan Group’s article here

These are stunning figures, this administrative overhead isn’t just annoying — it’s expensive. Every hour spent chasing down a payment or fraud attempt is an hour not spent serving customers, closing sales, or building your business.

Growth Delayed or Canceled

Growth Delayed or Canceled

Growth Delayed or Canceled

Growth Delayed or CanceledMore than 89% of business leaders say extended payment terms have disrupted long-term growth goals. That means expansion plans are delayed. New hires are postponed. Opportunities are missed.

Even more concerning, 26% of businesses have ended partnerships over persistent payment delays. These aren’t just inconveniences — they’re cash flow disruptors that poison otherwise strong business relationships.

Late payments create tension, introduce doubt, and reduce the willingness to take strategic risks. When you can’t count on getting paid, you hesitate to invest.

Understanding the Psychological Drivers Behind Late Payment Methods

Understanding the psychological drivers behind late payment practices can help businesses aiming to mitigate financial risks in 2025.

Factors such as the fear of negative feedback or the desire to preserve cash flow, may lead decision-makers to prolong payment cycles. Additionally, the emotional landscape of business relationships plays a significant role; clients might delay payments due to perceived inequalities in service or value.

Recognizing that these delays can stem from psychological insecurity rather than sheer negligence is key. By fostering open communication and building trust, companies can not only predict but also actively address these psychological triggers, reducing the incidence and impact of late payments on outstanding invoices.

Attention Before Automation

Despite growing awareness, many small businesses are caught between legacy payment practices and the pressure to automate. Nearly 91% still rely on checks, and only 17% have fully automated their accounts receivable processes.

According to Dean Kaplan in his article on the late payment crisis: 91% of organizations still utilize checks, up from 75% in 2023.

That sharp rise in check use — up from 75% in 2023 — isn’t just habit. It reflects the practical trade-offs smaller businesses face:

- Economic uncertainty pushes many toward “slower” payments that give them more control over cash flow.

- Rising digital invoicing fees make checks look like the cheaper option — even if they aren’t in the long run.

- Legacy payment systems and uneven tech adoption keep paper payments alive.

- Some decision-makers still perceive checks as safer, despite the data.

- And after the pandemic’s big tech push, many hit transition fatigue — and fell back on familiar payment processes.

So while fraud risk is rising, many businesses are simply doing what seems most manageable for their size. For many smaller companies, the cost and complexity of automation may not pencil out.

Monitoring and Analyzing Customer Payment Behavior

By leveraging data analytics and payment history, companies can identify patterns and trends that highlight how much time clients take to pay. This enables businesses to engage early intervention processes like adjusting payment terms, additional payment options such as payment plans and early payment incentives.

It also empowers them to have more informed discussions with clients about their accounts. Regularly reviewing payment behaviors can reveal underlying issues, such as cash flow struggles on the client side or dissatisfaction with service. Moreover, proactive communication based on these insights can foster stronger relationships, improve trust, and ultimately, enhance the likelihood of payments. As companies invest in real-time monitoring, they will be better equipped to respond swiftly to payment delays, ensuring that their financial health remains intact and that they can focus on pursuing growth opportunities instead of constantly battling overdue invoices.

Back to the payment crisis

The real story behind this shift isn’t checks, software, or even technology — it’s the late payment crisis of 2025. For small businesses, delayed payments aren’t just frustrating — they’re destabilizing.

When overdue accounts pile up and outstanding payments linger past the payment due dates, the effects ripple quickly:

- Cash flow tightens, making it harder to meet payroll, order materials, or plan ahead.

- Processing and follow-up costs rise, draining already thin margins.

- Payment fraud risks climb, sometimes requiring legal action another cash flow drain.

- And without structure, tracking and escalation turn into constant fire drills instead of a controlled process.

This crisis isn’t theoretical — it’s already happening. More businesses are falling behind on overdue payments, and many lack a clear payment process to deal with it. Checks, manual invoicing, and ad hoc collection methods make the situation worse, not better.

That’s where attention and structure make the difference. A well-defined accounts receivable system gives business owners clarity: who owes what, how long it’s overdue, and what happens next. It puts control back in their hands without forcing them to overinvest in technology they may not need.

Why Structure Beats Blind Automation

Why Structure Beats Blind Automation

Why Structure Beats Blind AutomationThis isn’t a technology problem — it’s a structure problem. If your AR system isn’t clearly defined, automating it just makes the mess move faster.

Before layering on software, what matters most is intentional design: clear payment terms, timely reminders, structured escalation, and predictable follow-through.

That’s where Cash In USA comes in. We help businesses build that structure — and only add automation where it truly creates value. Our approach includes:

- Clear payment terms and upfront agreements

- Defined reminder cadences for upcoming and overdue invoices

- Tiered escalation strategies that shift tone and urgency appropriately

- Real-time visibility into who owes what — and for how long

- Consistent follow-through, no matter the volume or season

Once this foundation is in place, smart automation can amplify results — without draining limited budgets or overwhelming small teams.

AR as a Growth Lever — Not a Back-Office Task

A structured receivables process turns uncertainty into predictability. Businesses that focus on clarity and consistency see:

- Faster payments

- Lower processing and collection costs

- Fewer write-offs and less bad debt

- Stronger customer relationships built on clear expectations

- More accurate forecasting for growth

When you know what’s coming in — and when — you run your business with more control and less stress.

Bottom Line

Late payments aren’t just inconvenient. They quietly erode cash flow, increase risk, and limit growth. But the solution may not be to throw software at the problem.

Attention before automation means getting the structure right first — then automating only what makes sense for your size and strategy.

✅ Key Takeaway: Late payments aren’t just a nuisance. They’re a barrier to growth, a drag on productivity, and a preventable threat to your bottom line.

✅ Key Takeaway: The smartest AR systems start with structure, not software.

🚀 At Cash In, we help small and midsize businesses turn overdue invoices into consistent cash flow. Whether you need help with automation, reminders, or full-service collections, we’re ready when you are. Let’s talk.