How to Send an Overdue Bill to Collections

Updated for 2024

I was recently surprised by the question, “How do I send an overdue bill to collections?” I’d forgotten that not everyone knows what to do or how to send a past due balance or a bad debt to a collection agency. So, first I’ll tell you how to do it – and then I’ll tell you a bunch of other stuff about it so that Google shows you my post – okay?

I was recently surprised by the question, “How do I send an overdue bill to collections?” I’d forgotten that not everyone knows what to do or how to send a past due balance or a bad debt to a collection agency. So, first I’ll tell you how to do it – and then I’ll tell you a bunch of other stuff about it so that Google shows you my post – okay?

How to Send an Overdue Bill to Collections

Like most things, it depends on the agency, but all agencies will ask you to set up an account and to provide them with information about both the debtor, the debt, and the creditor. You are the creditor, and the customer is the debtor, and of course, the debt is the money that is owed. This is generally done with an online form.

To submit an account for collections to Cash In is a simple 4-step process.

- Click this link https://cashinusa.com/plans-and-pricing/ to select your plan and pay for it. Unlike traditional collection agencies, we charge a nominal fee to collect your bad debt account, which provides several benefits to both you and us. I describe the differences between flat-fee (our model) and contingency collections (traditional model) below.

- Once you’ve paid for your package, you’ll receive an email acknowledging receipt of the payment. Within that email, there will be a link that says ‘Submit Accounts Here.’ Click the link and fill out the form that opens.

- Upload your documentation (optional) – you can read more about documentation here.

- Click submit at the bottom of the form

Honestly it’s that easy. If you get confused or have questions click here to send me an email or give me a call at 800-201-CA$H (2274) my extension is 110.

Now, on to some other questions you might have.

What does “turn an account over to collections” mean?

Turning an account over to collections, or sending a bill to collections, simply means hiring a third-party collection agency to recover either outstanding invoices, medical debt, credit card debt, unpaid rent, and even personal loans that have gone unpaid.

Why Use a Collection Agency?

The decision to use a collection agency is a strategic decision that may or may not be right for you or your small business. Here are several reasons why it might be a good idea:

- Expertise and Experience: Collection agencies specialize in debt recovery, employing experienced professionals who understand the legalities and best practices involved. They are familiar with various debt collection techniques and know how to navigate complex situations.

- Time and Resources: Pursuing late invoices and other unpaid bills is a time-consuming and resource-intensive process. For businesses with limited staff or individual creditors with no experience in the debt collection process, outsourcing this task to a collection agency can often be a huge relief.

- Improved Cash Flow: Unpaid debts can significantly impact cash flow, especially for small businesses or individuals that rely on timely payments. Working with a collection agency increases the chances of recovering outstanding debts, thus improving overall financial stability.

- Legal Compliance: Collection agencies are well-versed in debt collection laws and regulations, ensuring that the recovery process adheres to legal guidelines. This helps mitigate the risk of legal disputes or repercussions associated with improper debt collection practices.

- Professional Communication: Collection agencies employ trained professionals (usually) who are skilled in effective communication and negotiation techniques. They are tasked with maintaining a professional demeanor while engaging with debtors, reducing the emotional burden on creditors, and preserving relationships when possible.

- Increased Success Rates: Collection agencies have access to advanced tools and databases that facilitate the location of debtors and the assessment of their ability to repay. This enhances the chances of successful debt recovery relative to individual efforts.

- Preserve Business Reputation: Handling unpaid invoices or debts professionally through a third-party agency can help protect your business and personal reputation. It avoids direct confrontations or strained interactions with debtors, maintaining a positive image in the market.

- Cost-Effectiveness: While collection agencies charge a fee for their services, the potential benefits, including time saved, improved cash flow, and successful debt recovery, often outweigh these costs. It can be a cost-effective solution in the long run.

- Focus on Core Activities: Outsourcing debt collection allows businesses and individuals to focus on their core activities, such as business growth, customer service, or personal priorities, rather than being consumed by debt recovery efforts.

When Should You Send an Overdue Bill to Collections?

I’m not going to say “it depends” , because it doesn’t. The fact is, the older an invoice gets the harder it will be to collect the overdue payment. More than one broken promise? You have a problem.

For best results turn your delinquent accounts over between 90 and 120 days, For ANY results turn your past due accounts over at 180 days, that’s about 6 months. Over 18 months and your expectations should decline as will your results, but the unpaid debt is still collectable.

How Late is Too Late? (and I’m just going to give them one more chance)

*If I only had a nickel … sigh

Sometimes just telling your delinquent customer you’re going to turn his account over to collections will produce results. But if it doesn’t work the first time there is no reason to believe it will work on subsequent attempts. A key benefit of working with a flat-fee collection agency such as Cash In is that you won’t pay the 30% to 50% commission traditional collection agencies charge. So there really is no good reason to wait. For a nominal up-front fee you can improve your chances of collecting your past due invoice by submitting it between 90 and 180 days.

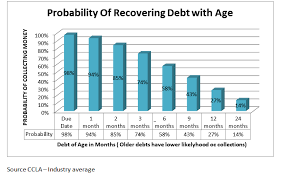

Debt Collection Recovery Rates

At 90 days, the average recovery rate for a 3rd party debt collection agency is around 73%. So if your customer isn’t paying and you turn it over for collections you’ve got a better than average chance of collecting. But 90 days is very aggressive and, in my opinion and that of most professional debt collectors, in most cases premature. I discuss what to do before you call an agency below.

Thirty days later at 120 days, the average collection rate drops to around 64%, still better than average. At this stage you should have already taken a number of steps internally to collect. Including calls, emails and if they are unresponsive a past due notice or in-house collection letter warning them of the consequences of non-payment. Letting them know you’re considering sending their invoice to a collection agency is often enough to generate at least a response and very often payment.

At 180 days, or about 6 months the average recovery rate falls further to around 57%, and every month thereafter it goes lower and lower. There are industry averages and results can vary significantly depending on the circumstances. Things that might make an overdue balance harder to collect include:

The Industry: Some industries have much higher bad debt ratios than others. Such as:

- Healthcare

- Retail

- Subscription Based Businesses

If you are in one of these industries your should turn your accounts over sooner (120 days) rather than later to maximize results.

Geographic Region: There are a number of geographic factors that may impact your ability and an agencies ability to recover your debt, such as:

- Regions experiencing economic downturns such as business, closures and job losses

- Income levels and wealth disparities. Areas where a large portion of the population fall below the poverty line will have reduced levels of debt recovery

- Industry concentration – Regions with a heavy concentration of industries known for higher bad debt, like those we mentioned above

- Regulatory Environment – Differences in regulations related to debt collection practices, credit reporting and consumer protections will also influence bad debt levels regionally (think California).

Economic conditions overall: (Think pandemic)

The circumstances of the particular balance due:

- Disputed?

- Invoiced very late?

- Invoiced incorrectly?

Of course the agency you choose will have some impact as well, but not as much as you might think. Like most industries a good collection agency may be hard to find. You might want to check with your local Better Business Bureau before choosing. There are some bad agencies out there, but most will do the best they can with what you give them. Their reputation and income depend on them doing a good job and most do.

Before You Turn to a Collection Agency:

Fair and Reasonable Win the Game

While we encourage you to submit overdue accounts before it is too late to collect them, the cost of 3rd party collections is high, as is the risk of losing customers. Customers are sensitive and the use of a collections agency could damage your relationship with your delinquent client, which could have long-term consequences for future business opportunities. So before you turn to outside collections:

Ask Your Customer to Pay

Sometimes all it takes is a friendly phone call and a copy of the overdue invoice to collect your late payment. Make sure you have a plan in place to either email or call delinquent customers, and that your plan has been executed before turning to an agency.

Give Fair Warning

If they aren’t responding to your emailed payment reminders, pick up the phone and call, and if that doesn’t work send a letter. Attach the pdf copy of the letter to an email and put another copy into the regular mail. Let them know you’re considering using an agency, at least 30% of the time that is enough to get payment.

What About a Payment Plan?

If your customer offers a payment plan, work with him. If they don’t ask, and the balance justifies it, offer one. But ask for more than they offer, they’ll probably offer less than they can handle and you would be remiss if you didn’t at least try.

Make it Easy to Pay

Customers today expect financial transactions to be seamless. Offer multiple payment options including credit and debit cards, ACH, mobile wallets, Paypal, Zelle – there are more but you get the idea. Reduce friction to improve your internal success rate and get paid faster.

Escalate to the Controller, Owner, Husband or Wife

If you’re collecting a business debt and accounts payable isn’t responding escalate to the controller or if it’s a small business the business owner. If you’re collecting a consumer debt reaching out to the other partner i.e. husband if you’re talking to the wife or wife if you’re talking to the husband will often get things moving.

Make sure you let them know you’re planning to take further action that your next step may include reporting to the credit bureau, or possible legal action. In other words try everything you can think of, short of harassment. The goal is to avoid collection if at all possible.

If None of That Works ..

It’s probably time to try a third party. Once you’ve made the decision to use a collection agency to collect an outstanding balance, you’ll need to choose one. As of this writing, there are over 7000 collection agencies in the US. It’s an 18 billion dollar industry. So you’ve got a lot of choices. Obviously, we hope you choose us, but here are some things to consider.🙂

Flat-Fee or Contingency?

When choosing a debt collection agency you’ll need to choose the pay structure that is appropriate to the debt you’re trying to collect and your needs and desires.

Flat- Fee Collections

Flat-Fee agencies such as ours, Cash In USA, Inc, charge a nominal flat fee up-front and no commission on the back end. The upside is, if they/we are able to collect you’ll save the 20% to 50% commission traditional no collection, no fee agencies charge. The downside is, there is no refund if the money isn’t collected. You’re paying for services rendered not results.

Flat-fee is inappropriate for highly disputed balances and accounts that haven’t been submitted in a timely manner. So, if you’ve been sitting on it for two or three years contingency might make more sense.

Cash In is a Flat-Fee collections agency, we discuss the benefits in depth here. We have an average 46% recovery rate and when it doesn’t work you have the option of transferring your accounts to contingency collections.

Contingency Collections

Contingency collection agencies work on a no collection, no fee basis. So, their fee is “contingent” on them getting paid. The upside is, you don’t have to pay if they are unable to collect. There downside is – you may have a hard time finding an agency that will accept your account if the balance is too low, if it’s not a commercial account or if you don’t have ongoing work. Additionally, contingency collectors, can be overly aggressive and at times abusive, destroying any possibility of an ongoing business relationship with your customer after the debt is collected and sometimes sparking complaints, lawsuits and regulatory fines.

Research and Due Diligence

It’s simple enough to look up reviews. Almost all agencies will have some poor reviews, but if the preponderance of reviews are bad move on. If there are no reviews at all, you might want to move on.

Talk to other business owners, property managers and freelancers who have had to use an agency to see if they can recommend a good agency.

Once you’ve got a short list you might want to check with your local Better Business Bureau to see if the agency you’ve chosen has received complaints. A couple of complaints shouldn’t be considered a big deal. Most agencies will have one or two. But if there many, again you might want to move on.

And finally call the agency you’re considering. See if they are willing to answer your questions and if you feel comfortable with the conversation you have. Beware of anyone promising results. Debt collectors aren’t fortune tellers, and until they get your debtor on the phone they don’t know what is going to happen. That said a good collector may be able to give you some idea of collectability after listening to your story.

Summary

We’ve done our best to show you not only how to send an overdue bill to collections, but also how to strategically choose the best agency for you and your debt. If you have a question we haven’t answered you can check out our FAQ’s here or, leave a comment. You can also fill out our Ask a Question Form here, or call Vienna directly at 800-201-CA$H (2274) x110.

*What does the saying if I had a nickel mean?

“If I had a nickel for every time”, implies that the situation has happened a lot to the person. In this case, If I had a nickel for every time I’d been told I’m just going to give them one more chance, I’d have a very heavy piggy bank🙂