How old is too old?

As is often the case, it depends (again!). Each state has its own statutes governing the amount of time you have to sue a debtor. Once the statute date has passed your debt is considered to be time-barred and while in many cases you can continue to try to collect you can not sue, you’ve lost your leverage and nearly eliminated your chances of success, many agencies won’t be interested in taking your case at this point.

However, all is not necessarily lost. Even if the state statute for your debt has passed, you may be able to credit report your debtor. Most bad debts can be credit reported for up to 7 years, adding, in some cases, another 3 years to the amount of time you can have a negative impact on your debtor’s credit report. This is often enough to convince a debtor to try to get you paid.

Often, but not always, the timer starts from the last time your customer or debtor made a payment. This is one reason a debt collector might accept what appears to be an absurdly small payment, they’re often trying to restart the clock! Again, this varies from state to state, and laws constantly change.

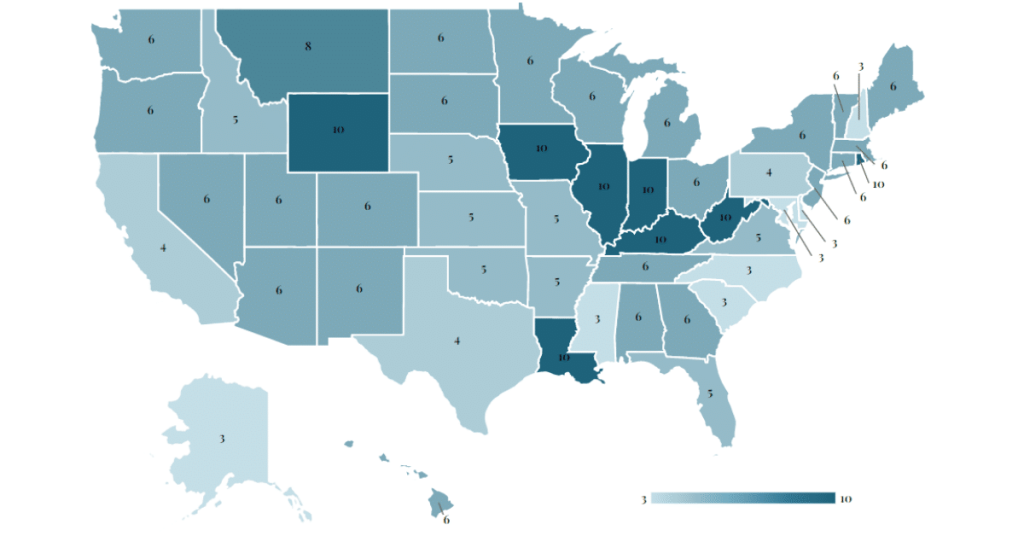

The chart provided here gives you a state-by-state summary of the statutes governing delinquent debt. Please note: This is not legal advice. The information provided is the most accurate information we could find at the time we published it; however, there may have been changes since. Please consider this to be a guideline. For the most accurate and up-to-date information, check with the State Attorney General in which your debtor resides, not necessarily the state in which the debt was incurred.

| State | Written Contract | Oral Contract | Promissory Note | Open Account | §§ |

|---|---|---|---|---|---|

| Alabama | 6 | 6 | 6 | 3 | § 6-2-34 |

| Alaska | 3 | 3 | 6 | 3 | §45.03.118 |

| Arizona | 6 | 3 | 6 | 3 | § 12-548 |

| Arkansas | 5 | 3 | 5 | 3 | § 4-3-118 |

| California | 4 | 2 | 4 | 4 | § 16-56-111 |

| Colorado | 6 | 6 | 6 | 6 | §13-80-101.5 |

| Connecticut | 6 | 3 | 6 | 6 | §§13-80-103-5 |

| Delaware | 3 | 3 | 3 | 3 | §§52-576 |

| DC | 3 | 3 | 3 | 3 | §§10-181 |

| Florida | 5 | 4 | 5 | 4 | §§95-11 |

| Georgia | 6 | 4 | 6 | 4 | §§9-3-24 |

| Hawaii | 6 | 6 | 6 | 6 | §§657-1 |

| Idaho | 5 | 4 | 5 | 4 | §§5-216 |

| Illinois | 10 | 5 | 10 | 5 | §§5/13-205 |

| Indiana | 10 | 6 | 10 | 6 | §§34-11-2-11 |

| Iowa | 10 | 5 | 10 | 5 | §§614.1 |

| Kansas | 5 | 3 | 5 | 3 | §§650-11 |

| Kentucky | 10 | 5 | 10 | 5 | §§413.160 |

| Louisiana | 10 | 10 | 5 | 3 | §§3499 |

| Maine | 6 | 6 | 6 | 6 | §§752 |

| Maryland | 3 | 3 | 6 | 3 | §§5-101 |

| Massachusetts | 6 | 6 | 6 | 6 | §§260-2 |

| Michigan | 6 | 6 | 6 | 6 | §§600.5807 |

| Minnesota | 6 | 6 | 6 | 6 | §§541.05 |

| Mississippi | 3 | 3 | 3 | 3 | §§15-1-49 |

| Missouri | 10 | 5 | 10 | 5 | §§516.110 |

| Montana | 8 | 5 | 8 | 5 | §§27-2-202 |

| Nebraska | 5 | 4 | 5 | 4 | §§25-205 |

| Nevada | 6 | 4 | 6 | 4 | §§11.190 |

| New Hampshire | 3 | 3 | 6 | 3 | §§381-A:30-118 |

| New Jersey | 6 | 6 | 6 | 6 | §§2A:14-1 |

| New Mexico | 6 | 4 | 6 | 4 | §§37-1-3 |

| New York | 6 | 6 | 6 | 6 | §§213 |

| North Carolina | 3 | 3 | 5 | 3 | §§1-52 |

| North Dakota | 6 | 6 | 6 | 6 | §§28-01-16 |

| Ohio | 8 | 6 | 6 | 6 | §§2305.06 |

| Oklahoma | 5 | 3 | 5 | 3 | §§12-95 |

| Oregon | 6 | 6 | 6 | 6 | §§12.080 |

| Pennsylvania | 4 | 4 | 4 | 4 | §§5525 |

| Rhode Island | 10 | 10 | 6 | 10 | §§9-1-13 |

| South Carolina | 3 | 3 | 3 | 3 | §§15-3-530 |

| South Dakota | 6 | 6 | 6 | 6 | §15-2-13 |

| Tennessee | 6 | 6 | 6 | 6 | §§28-3-109 |

| Texas | 4 | 4 | 4 | 4 | §16.004 |

| Utah | 6 | 4 | 6 | 4 | §§7B-2-309 |

| Vermont | 6 | 6 | 6 | 6 | §§12-511 |

| Virginia | 5 | 3 | 6 | 3 | §§8.3A-118 |

| Washington | 6 | 3 | 6 | 3 | §§4.16.040 |

| West Virginia | 10 | 5 | 6 | 5 | §§55-2-6 |

| Wisconsin | 6 | 6 | 10 | 6 | §§893-43 |

| Wyoming | 10 | 8 | 10 | 8 | §1-3-105 |