Collecting Accounts Receivable, A Practical Guide

What are Accounts Receivable Collections?

Accounts receivable collections is the process of managing and collecting payments from customers who have purchased goods or services from a business, freelancer or professional service provider, and have outstanding, typically overdue invoices. Outstanding invoices means unpaid or open invoices.

Your collections process should include a system for contacting customers to ask for payment of invoices with payment terms that have not been met, either by email, mail, text, phone or fax (yes, fax is still a thing but they usually land in your email inbox now), negotiating repayment terms, or even taking legal action or turning to a collection agency to recover the debt. However, the purpose of an effective accounts receivable management system is to avoid the need for such extreme measures.

Accounts receivable represents the amount of money owed to the company by customers for products or services that have been provided but not yet paid for. It is recorded as a current asset on the company’s balance sheet, reflecting the funds expected to be received in the near future. Managing accounts receivable collections is crucial for businesses to ensure a steady cash flow that supports day-to-day operations. By promptly collecting accounts receivable payments within a specified timeframe, ideally under 60 days, companies can strengthen their cash flow and maintain financial stability.

Accounts receivable collections is a vital part of running a business. It helps to ensure that bills are paid in a timely manner so that cash flow is maintained.

We read the following in someone else’s accounts receivable collections blog post:

“Effective accounts receivable collections can be challenging, and it is important to remember that every customer is different and that there is no one-size-fits-all approach. By taking the time to understand each customer’s unique needs and circumstances, businesses can increase their chances of success”.

It sounds good, but my 30+ years of experience collecting accounts receivable has led me to believe this is NOT TRUE. In fact, in my opinion, by taking the time to understand each customer’s unique needs and circumstances, you’ll waste huge amounts of time and probably become too friendly with your customers, which almost always leads to trouble collecting.

The truth is, regardless of industry, personal circumstances, or individual personalities, an effective accounts receivable management system requires time, organization, diligence, professional courtesy, and an easy to use CRM, not understanding.

We’re looking for the answer to two questions when collecting accounts receivable. How much (i.e., how much will you be paying) and when (when will you be paying it)? Why someone isn’t paying only becomes important when and if they are disputing and refusing to pay. Inability to pay really doesn’t require your understanding of why either, though they’ll probably end up telling you whether you want to know or not.

I realize this may sound harsh, perhaps even heartless, but it’s true nonetheless. I don’t mean you should be rude or unkind, or unfriendly. I’m simply recommending you stick to the task at hand.

Accounts Receivable and Bad Debt Collection – What’s the Difference?

Accounts receivable collections and bad debt collections are NOT the same. Bad debt collections are undertaken when accounts receivable collection efforts have failed.

Accounts receivable collections are typically undertaken in-house (though some companies, such as ours, offer this service), while bad debt collections are generally handled by a debt collection agency (we do this as well).

All of the monies owed to a company, both current and past due, constitute the company’s accounts receivables.

Accounts receivable are owed by customers. Accounts receivable are good. The more accounts receivable we have, the more sales we’ve made. Accounts receivable become cash in the bank once they’ve been collected.

When Do Accounts Receivable Become Bad Debt?

Customers become debtors when they fail to pay their invoices. Accounts receivable become bad debt when customers become debtors.

When all of your accounts receivable collection efforts have failed to produce a payment, the invoice has become a bad debt. Most small business owners wait way too long to identify bad debt and turn it over to a bad debt collection agency. Waiting too long to turn your accounts over to a debt collection agency makes it more difficult, if not impossible, for the agency to collect them. While there are many variables to consider, here is a good rule of thumb;

Any undisputed invoice that has reached 180 days and remains unpaid is probably a bad debt.

Why Undisputed?

Disputes need to be resolved to get your invoice paid. Demanding payment for invoices with unresolved disputes rarely works. It’s not uncommon to find both creditor (you) and debtor (your customer) refusing to negotiate or be reasonable when disputes occur. Everyone gets ticked off, and the creditor sends the invoice to the big bad collection agency to get them to bully the customer into paying. This is a very poor use of everyone’s time, and more importantly, it rarely works.

How to Resolve Disputed Invoices

- Be certain you understand the issue – what is your customer’s beef? It’s unproductive to demand payment without listening to the customer’s complaint.

- Investigate – were errors made? Were you late? Did you make promises you couldn’t keep? If so, on to step 3 …

- Take responsibility for your side of the problem. Disputes don’t generally happen in a vacuum. If you blew it, even a little bit, admit it. Most of the time, your customer will become more reasonable when you do.

- Be reasonable – if your customer has a legitimate complaint and is asking for a reasonable accommodation, cooperate. Always remember 80% of something is better than 100% of nothing.

- Don’t be a chump. If the dispute is not reasonable, and your customer is just trying to get away without paying, call an agency, preferably ours, and see if they/we can help. And finally …

- File suit if necessary and as a last resort. You can secure your claim with a monetary judgment which is good for 10 years and renewable for 10 more in most states.

There are a number of things you can do to improve your in-house collection results so you can avoid everything we just talked about – here are some ideas:

1. Do Your Due Diligence

Make sure your customer is creditworthy before offering terms.

2. Ensure Invoices Are Clear and Error-Free

Be certain your invoices are clear, error-free, sent on time, and to the correct email or address. The reasons we hear most often while collecting late payments for our customers are missing invoices and invoicing errors.

3. Systematize Your Collection Process for Better Cash Flow

All processes benefit from systematization. AR collections are no exception. Implementing a structured and diligent collections process can avoid financial instability.

4. Use a CRM

It’s important to document all of your collection efforts, so you can:

- Improve your results – by documenting what was said and what promises were made, you’ll be better able to identify next steps.

- Use your documentation in court to prove your case should you ever have to file suit.

- Write off the bad debt. The IRS will want proof that you tried to collect; your documentation will do the trick if you write complete but concise notes.

5. Schedule Your Follow-Up and Do It On Time

Making one call or sending one email and then doing nothing for a month actually teaches your customer to ignore you. Be sure to always get in touch the day the account is overdue. For new clients or clients who often pay late, a reminder email or duplicate e-invoice can help.

6. Communicate Frequently

There are three main reasons for delayed payment:

- Your customer simply forgot about the invoice.

- Your customer has an issue with the invoice amount or the product/service provided. Instead of communicating this to you, they just don’t pay the invoice. You will only find out if you get in touch.

- Your client is also waiting for payment and is trying to extend credit/preserve cash.

It’s human nature to want to “do the right thing.” People will usually pay suppliers who are in touch on a regular basis and ask for payment. Call, text, or email your clients at appropriate intervals.

7. Send Monthly Statements

They work. Use automation if your software supports it. Most software packages do these days. You can also set automatic reminders before, on, and after the due date to facilitate payment.

8. Contact Everyone with a Past-Due Balance

Not just those with high balances. “Good accounts” need to be contacted if they have overdue accounts as well as those you consider not as good.

9. Make It Easy for Customers to Pay

To maintain healthy cash flow, offer as many payment methods as you can. Encourage clients to pay online or over the phone or commit to a payment date.

10. Consider Outsourcing or Hiring AR Specialists

AR is a specialized function that requires specific systems and skills. Whether you have your own AR staff or use an outsourced AR service, make sure staff are:

- Polite and professional.

- Communicate with customers at appropriate intervals.

- Document all client conversations for history and traceability.

11. Make Invoice Collection and AR Management a Key Performance Metric

Business growth and survival correlate to cash flow and speed of invoice collections. You should not need to scramble for payroll or put off purchasing new equipment because your customers owe you money.

To make accounts receivables a key performance metric:

- Schedule a short meeting once a week dedicated to analyzing outstanding debtors.

- Measure “Days sales outstanding” (DSO) and set a target for reducing this key metric. DSO is used to calculate the average collection period.

- Use accounts receivable management software to benchmark your performance.

- Celebrate actually getting paid just as much as you celebrate making a sale!

12. Exercise Caution with Early Payment Discounts

One we don’t recommend is discounts for early payment – at least not across the board. Too many customers will take the discount and not pay early – so use this judiciously if at all.

For Vienna’s Top Ten Tips, Tricks, and Techniques for Getting Paid Faster – click here.

How to Measure Accounts Receivable Collection Effectiveness

If you type this question into Google, you’ll find articles listing as few as 4 and as many as 11 methods of measuring your effectiveness in collecting your receivables. We think 11 is a bit much and probably too much work for the average business owner to keep up with. But you do need to know if your efforts are producing the intended result. So let’s look at the top 3 metrics for measuring collection performance.

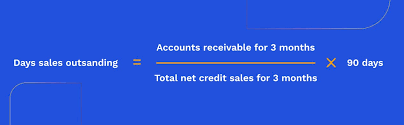

Days Sales Outstanding or DSO

Days sales outstanding measures the average number of days from invoice to money in the bank. It is a measure of how long it takes a company to collect payment after a sale has been made and how quickly a company’s receivables turn into cash.

A high DSO can be a sign that a company is having difficulty collecting payments, which could lead to financial distress down the road. Conversely, a low DSO could indicate that a company is too tight with its credit terms, which could make it difficult to grow sales.

DSO is used by both creditors and investors to assess a company’s financial health. DSO is just one metric to consider when evaluating a company’s financial health, but it’s an important one to keep an eye on.

To calculate DSO, divide your current AR balance by your credit sales in the period you’re measuring, then multiply that by the number of days in the measured period.

Link to this video is in the copy

Average Days Delinquent or ADD

The average number of days that a delinquency remains unpaid is known as the Average Days Delinquent or ADD. ADD measures how long, on average, it’s taking your customers to pay. A low number means your customers are paying relatively quickly. A high number means they are taking longer to pay. Lower is better.

The first step to reducing your ADD is setting up collection procedures to deal with your delinquent accounts, the second step is using the procedures you set up!

Accounts Receivable Turnover Ratio

The accounts receivable turnover ratio measures how quickly your company collects payments from its customers. To calculate the ratio, you divide your company’s total sales by its average accounts receivable. The higher the ratio, the better – a high turnover ratio means that your company is efficient at collecting its receivables, while a low ratio could suggest that your company is extending too much credit or your collection processes are inefficient and a review of your collection strategies may be needed.

Let’s look at one more ratio –

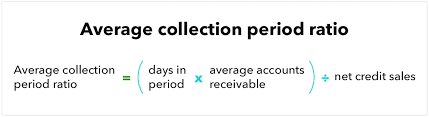

Average Collection Period

The average collection period is the number of days it takes for a business to receive payment after making a sale. Again, this ratio is used to measure the efficiency of a company’s credit and collection policies. A low average collection period indicates that a company is collecting payments quickly, while a high average collection period suggests that payment collections are taking longer than expected.

The ideal situation is to have an average collection period that is in line with the company’s credit terms. For example, if a company offers its customers 30 days to pay, then the average collection period should be between 30 and 45 days. If it takes much longer than that, it may be an indication that the company’s credit and collection policies need to be reviewed.

As we discussed at the beginning of this section, it isn’t necessary to use all of these metrics but you should choose one, or probably two so you can compare them and be certain you know how well your accounts receivable department is performing.

Collections by Industries

One more way to evaluate your company’s effectiveness in collecting accounts receivable is to compare your metrics to those of others in your industry. Unfortunately, that information isn’t easy to find, but Dunn & Bradstreet is a good place to start.

Summary

In summary, small businesses need to set up a system for collecting accounts receivable. The receivable collection process begins with an appropriate credit analysis that helps identify accounts receivable risks, billing on time and correctly, and systems to improve collections.

Next, develop a plan to collect receivables using your receivable aging report and multiple collection methods, including payment reminders via letters, phone calls, and email notifications. Use various payment options, including ACH, credit cards, pay by phone, web-based payment, and payment plans, to collect past-due invoices.

Finally, track your collections performance regularly using at least two commonly used metrics, and whenever possible, compare your results to others in your industry so you can measure the effectiveness of your collection strategy.

Need Help?

We can help in three simple ways:

- Done-for-you AR collections (even if you only have one or two late payers).

We handle the follow-up, so you can stay focused on the work that gets you paid. - Set up a system and train your staff to use it.

We’ll give you the scripts, tools, and tracking methods to make it easy to manage in-house. - Escalate past-due accounts to bad debt collections when needed.

Our flat-fee demand Letter Packages make it easy to take the next step without giving up control.

Questions? Book a free, no obligation meeting here: https://calendly.com/cashinusa/15min

or just call me – if I’m at my desk I’ll pick up (800) 201-CA$H (2274)