Credit Collection Policy & Preventing Bad Debt

Credit Collection Policy & Preventing Bad Debt

Collection Prevention Part 4

Well, here we are. I promised to discuss your credit collection policy in the first email in this series. I saved it for the end (almost) because I know it’s boring, and you almost certainly think it doesn’t apply to you. But it’s important if you’re serious about preventing bad debt, and it’s not that big of a deal.

Think of a credit policy as a roadmap for your financial decisions. By setting these guidelines in advance, you can avoid making hasty choices during critical moments, such as a major sale or a cash flow crisis.

Think of a credit policy as a roadmap for your financial decisions. By setting these guidelines in advance, you can avoid making hasty choices during critical moments, such as a major sale or a cash flow crisis.

Why You Need a Credit Policy

Even if you think you don’t.

Reduction of Bad Debts: A structured policy, if implemented, not only helps identify potential credit risks early but also empowers you to take necessary actions to mitigate them. This proactive approach significantly reduces the likelihood of non-payment and bad debts, which can otherwise severely impact the financial health of your business, regardless of its size.

For a more detailed understanding of why a credit policy is essential and how to create one, I encourage you to take these two steps:

- Finish reading this article

- Download this resource – How to Create Your Credit Policy Step-by-Step.

More Reasons You Need a Credit Policy

Just in case you aren’t convinced here are a few more reasons for your to consider.

Cash Flow Management: Consistent cash flow is critical for a small business’s operations. A credit collection policy helps ensure timely payments, reducing the risk of cash flow disruptions that can affect the ability to pay bills, purchase inventory, and meet payroll.

Customer Relationship Management: A transparent and fair credit collection policy is not just about money; it’s about maintaining positive customer relationships. It sets clear expectations for payment terms and procedures, helping to avoid misunderstandings and disputes over payments. Clear expectations foster trust and goodwill with your clients, making them feel valued and respected.

Credit Risk Assessment: Your credit policy is your guide in evaluating customers’ creditworthiness before extending credit. By setting specific criteria for credit approvals, you can confidently minimize the risk of extending credit to customers who may be unable to pay, ensuring your business’s financial stability.

Legal Protection: If your credit policy includes terms and conditions that comply with legal requirements, it could protect your business should litigation become necessary.

Professionalism: A formal policy enhances a business’s professionalism. It shows that the business is serious about its financial practices, which can build trust with customers and suppliers.

Monitoring and Reporting: A well-written credit policy facilitates regular tracking and reporting of outstanding accounts receivable. Monitoring your accounts receivable helps identify late invoices early, allowing you to take corrective actions promptly.

Seems obvious enough right? And yet, most of the small business owners I’ve worked with don’t have one. It really doesn’t have to be a big deal, a simple 1 page document outlining your Credit Collection Policies and what you’ll do with past due invoices – and, very important, when you’ll do it – will suffice.

Setting Credit Limits and Payment Terms – You Need a Plan

Your plan begins with a couple of basic, essentially philosophical decisions. These decisions, rooted in your values and beliefs, will shape your credit policy. These are not arbitrary choices, but reflections of who you are and how you view the world, people, and business. If you make these decisions based on what you think you should do or what you read in a book or heard in a seminar, you probably won’t follow through with all the decisions that follow – this is your foundation, so keep it real.

Here are the two questions you and your credit manager need to consider;

- How strict will you be when extending credit?

- How flexible will you be when collecting delinquent invoices?

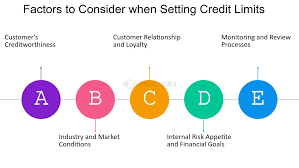

Extending Credit & Setting Credit Limits

If you’re strict about extending credit terms, you’ll spend less time collecting, but you may restrict sales. Conversely, if you extend credit liberally, you’ll sell more but spend more time on collections.

If you extend credit liberally to maximize sales, you’ll find you have more collection issues. That’s okay, but it requires a plan, i.e., decisions made in advance about how and when you’ll deal with late payers.

If you don’t consider credit at all or extend credit liberally and don’t make up for it with some good decisions about dealing with late invoices, you’ll have higher bad debt.

You’ll have costs in whichever business credit policies your choose. Either you spend the time and money upfront to check credit and make decisions congruent with your personal and business philosophy, or you spend the time and money to work with your customers, patients, or tenants when they can’t or won’t pay on time.

No choice is a choice for collection issues, higher bad debt, and, worst of all, lost customers.

Setting Payment Terms in Your Credit Policy

Establishing clear and effective payment terms in your credit policy is key to maintaining healthy cash flow and minimizing financial risks. Here’s a comprehensive guide to help you understand and set up robust payment terms that work for you and your customer.

Defining Business Credit Terms

Your business credit terms outline the conditions under which customers can purchase goods or services on credit. These terms typically specify the credit limit, payment due dates, and any applicable discounts for early payment. Clearly defined business credit terms ensure that both parties understand their obligations, fostering a transparent and efficient business relationship, and help in reducing the risk of late payments.

When setting payment terms, consider factors such as industry standards, the financial stability of the buyer, and your business’s cash flow requirements.

Following are some commonly used standard business payment terms, decide which are best for you and add them to your credit policy.

Most Common Terms

Net x Number of Days

The most common term we’ll typically see on an invoice is Net x number of days, with Net 30 being the most commonly used – however, it’s not uncommon to see Net 7, Net 10, Net 60, or even Net 90. Net simply means the payment is due within the number of days indicated from the invoice date so;

- Net 7: Payment is due 7 days from the invoice date

- Net 30: Payment is due 30 days from the invoice date

- Net 60: Payment is due 60 days from the invoice date.

You get the idea. These terms indicate the total time period the buyer has to pay the invoice amount without any penalties.

How to Write a Credit Collection Policy Step-by-Step

Due on Receipt

Payment is due immediately upon receiving the invoice. This term is often used for new customers until a relationship is established or smaller transactions to ensure quick payment and avoid unnecessary accounting costs.

Net End of Month (EOM)

Payment is due at the end of the month in which the invoice is issued. For example, if an invoice is issued on June 10th, payment is due by June 30th.

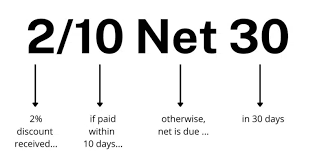

2/10 Net 30

This term offers an early payment discount. If the buyer pays within ten days, they receive a 2% discount on the invoice amount. Otherwise, the full amount is due in 30 days.

Other Common Terms

Cash in Advance (CIA)

Payment must be made before the goods or services are delivered. This term is common for international transactions or high-risk buyers.

Cash on Delivery (COD)

Payment is due at the time of delivery. This term ensures that the seller receives payment before transferring ownership of the goods to the buyer.

Monthly Billing

Invoices are issued at regular monthly intervals, often with payment due at a set date each month. This is common for ongoing services or subscriptions.

Stage Payments, Milestone, or Progress Payments

Payments are made in stages as certain milestones or phases of the project are completed. This term is often used in large projects or contracts. Most contractors and sub-contractors should be collecting progress payments.

Less Common Terms

Letter of Credit (LC)

A letter of credit is a financial instrument issued by a bank guaranteeing that the seller will receive payment from the buyer, provided certain conditions are met. This term is common in international trade.

Consignment

The seller provides goods to the buyer, who only pays for the goods once they have been sold to the end customer. Unsold goods can typically be returned to the seller.

Summary

Summary

Okay, even I’m getting bored with this. Let’s wrap this up.

Credit Extension

When deciding on your credit extension policy, consider your risk tolerance, cash flow position, and industry standards. This thoughtful approach, taken in advance, not only determines if you will extend credit but also how much, ensuring a secure and informed decision.

Not all orders are big enough to make a credit evaluation worthwhile. We suggest COD for new customers and small orders. You have to decide what small means for you. Our rule of thumb is, “Don’t extend more credit than you can afford to lose.” If you’re going to worry about it, don’t do it.

Terms

We’re all about cash flow and getting paid fast here, so we generally don’t recommend extended terms. Unless your industry calls for it, we suggest between net seven and net 30 days.

Collections Policy

When it comes to your collections policy, we advocate for the “Goldilocks Rule”, a balanced approach. Not too strict, not too flexible. We propose initiating collection efforts at around 10 days past the agreed terms, ensuring a fair and trusted relationship with your customers.

Write It Down

Write your decisions down, put a title on the paper you wrote it on, and file it with the rest of your SOP, ideally where you can reference it and use it for training. Voilà you have the beginnings of a Credit Policy:)

How to Write a Credit Collection Policy Step – by – Step available here.